The belief that the combination of GESY (Cyprus’s National Health System) and a standard hospital insurance policy offers total financial security is a trap that many fall into—until they are faced with a serious health crisis.

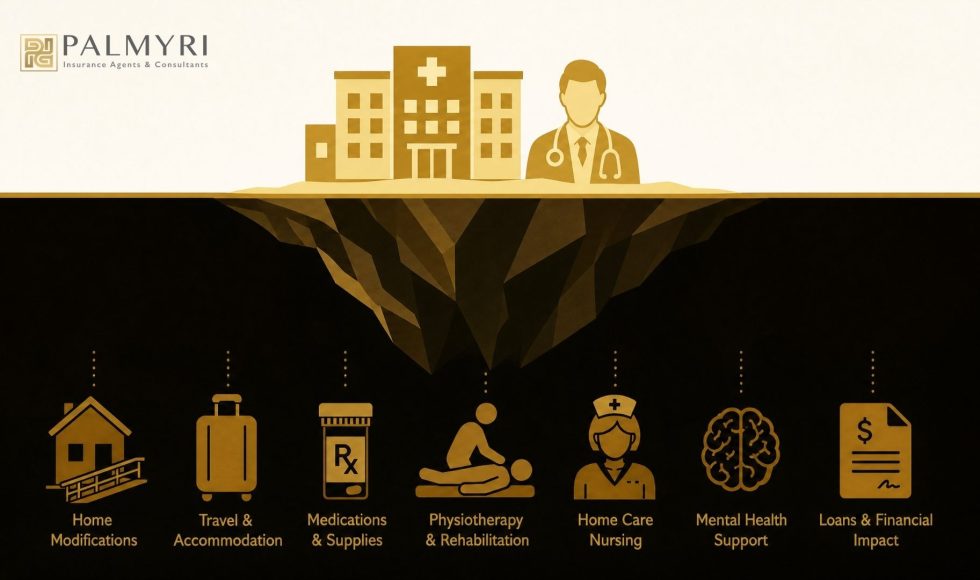

While the public health system and private health insurance focus on paying for the doctor, the surgery, and the hospital bed, a critical illness entails a series of “invisible” expenses that can dismantle a family’s financial foundations. These expenses do not concern the hospitalization itself but rather the patient’s survival and quality of life, and that of their loved ones, during and after treatment.

1. The Dramatic Loss of Monthly Income

The largest and most painful expense that no hospital program will cover is the replacement of income lost when a patient is forced to be absent from work for months or even years. GESY and health insurance pay the hospital, but they do not pay the rent, loan installments, school tuition, or daily bills that continue to pile up relentlessly.

The financial hemorrhaging caused by the inability of the primary breadwinner to work—or even a partner who must stay home to provide care—is a burden that only a critical illness lump-sum benefit can shoulder.

2. Travel and Accommodation Expenses for Specialized Treatments

Often, the best possible treatment for a serious condition is not available in the city or even the country where you reside, which entails enormous travel and accommodation expenses.

While insurance may cover the medical costs of surgery abroad, it will never cover airline tickets, hotel stays for relatives accompanying the patient, or extended living expenses in a foreign country. These amounts quickly add up to thousands of euros, creating an additional source of stress during an already difficult time.

3. Home Modifications and Specialized Equipment

A serious illness or a stroke can leave behind permanent or temporary mobility difficulties that require immediate changes to the living environment. The cost of installing a special ramp, renovating a bathroom for wheelchair access, or purchasing a specialized hospital bed and orthopedic aids falls entirely on the patient. Neither GESY nor hospital coverage provides funds to transform your home into a functional space that accommodates your new needs.

4. Home Care and Domestic Assistance

Returning from the hospital does not always mean full recovery, as many patients require daily support from a private nurse or home helper for their basic needs. This type of home-based service is considered social care rather than medical treatment and, as a result, is not covered by traditional health policies. The cost of someone to provide care, cook, and assist with the patient’s personal hygiene is a continuous expense that can deplete a lifetime of savings.

5. Experimental Treatments and Innovative Medicines

Medical science is evolving rapidly, but public systems and insurance protocols need time to incorporate new, groundbreaking treatments into their coverage. Many innovative drugs or genetic tests that can save lives are still considered experimental or have not been approved for full coverage by official bodies. In these cases, the patient faces the dilemma of paying the exorbitant cost of a treatment that may offer them hope out of their own pocket.

6. Long-term Rehabilitation and Psychological Support

The battle with a serious illness does not end with discharge from the clinic, as a long period of rehabilitation and psychological processing of the trauma follows. Countless sessions of physiotherapy, speech therapy, or intensive psychological support for the patient and their family often exceed the limits or time frames set by insurance companies. These post-hospital expenses are necessary for a full return to normalcy, but remain a personal financial obligation.

7. Loan Coverage and Ensuring Quality of Life

Finally, a serious illness does not stop obligations to banks or a family’s needs for a decent standard of living. Hospital programs ensure that you will get well, but they do not guarantee that after treatment, you will still have your home or that your savings will remain intact.

The need for a lump-sum capital to be used as you see fit—whether to pay off a loan or cover children’s tuition—is the only substantive answer to the financial uncertainty brought by a major health adventure.

Comprehensive Protection at Palmyri Insurance

At Palmyri Insurance, we understand that insurance is not just the purchase of a document, but the safeguarding of your peace of mind. We offer comprehensive coverage programs, including a critical illness policy that provides you with an immediate lump-sum cash benefit to cover all of the above expenses without restrictions.

Our approach is based on an in-depth consultative process, where your needs are analyzed fully and in absolute detail. This way, you have a clear picture from the very first moment of exactly what your policy covers and what it does not, so you can feel secure for any eventuality.

We are here to turn the complexity of insurance into an understandable and fair protection agreement for you and your family.